Ifrs 9 Arrangement Fees

On initial recognition a financial asset is classified into one of the three primary measurement categories. IFRS 9 including where relevant applying the Expected Credit Loss ECL model for impairment.

Hold To Collect How 2 Best Account It In Ifrs 9 Classification Of Financial Assets Annual Reporting

IFRS 9 and IAS 39 Fees and cost included in the 10 per cent test for derecognition of financial liabilities.

Ifrs 9 arrangement fees. In addition they can. So this is the terms. This was clarified by an amendment to IFRS 9 in the Annual Improvements to IFRS Standards 2018-2020 issued on 14 May 2020.

However IFRS 9 contains guidance on when cost may be the best estimate of fair value and also when it might not be representative of fair value. IFRS 9 will change the way many corporates account for their financial instruments. IFRS 9 is effective for annual periods beginning on or after 1 January 2018 with early application permitted.

The IFRS 9 model is simpler than IAS 39 but at a price the added threat of volatility in profit and loss. IFRS List Accounting Treatment of Arrangement fee paid to bank for term loan. The contract does not meet the definition of financial guarantee in IFRS 9 as the reference instrument in scope is a derivative.

4 Step 4 Allocate the transaction price to the performance obligations in the contract 90. Fee paid to lender in return for the lender committing to lend to borrower a certain amount and it is probable that the borrower will draw down the amount. IFRS 9 replaces IAS 39s patchwork of arbitrary bright line tests accommodations.

However if it is an increased interest rate on that loan then treat it under IFRS 9 but in practice if you will apply the penalty interest only in the next period not over all the loan term then basically you can just recognize it in profit or loss because it does not make a big. IFRS 9 paragraph B542. This standard required the classification and measurement of financial assets into only two categories.

Air value through other comprehensive income FVOCI. 41 Determine stand-alone selling prices 91 42 Allocate the transaction price 98 43 Changes in the transaction price 111. Amortised cost and fair value through profit or loss FVPL.

Applying IFRS 9 to related company loans can present a number of application challenges as they are often advanced on terms that are not arms-length or sometimes advanced on an informal basis without any terms at all. In October 2010 the IASB published the updated IFRS 9 2010 Financial instruments. Bank A earns a fee from this arrangement.

Commitment fees paid when it is probable that a loan will be originated should be treated as a prepayment and recognised as an adjustment to the loans EIR. Elimination of the held to maturity loans and receivables and available-for-sale categories. My client withdrew 20M at 01042018 at 05 2 reimbursed 20M at 01072018 withdrew 30M at 01102018 et 1 2 withdrew another 30M at 05 2 at 01012019.

The transaction costs were at 5M law advisory bank fees etc. Into and the loan commitment is not measured at FVPL. IFRS 9 para B543b.

All fees and points paid or received between parties to the contract that are an integral part of the effective interest rate IFRS 9B541 and transaction costs. The International Accounting Standards Board IASB is currently preparing a proposal to amend IFRS 9 with the aim of clarifying which fees should be included in the calculation for the assessment if a financial asset or liability is derecognized or not. Analysis The entity carries out the 10 test.

Contract often still can be measured at Amortized Cost. Borrower and lender the reference to fees in this context should refer to the fees between borrower and lender eg would not normally include fees paid a lawyer. Whereas above in the final step the fees.

D Loan syndication fees received by a bank that arranges a loan and retains no part of the loan package for itself or retains a part at the same EIR for comparable risk as other participants are within the scope of IFRS 15. Youll need to consider the new requirements for To help you drive your implementation project to the finish line weve pulled together a list of key considerations that many corporates need to focus on. This has resulted in.

If it is a fixed fee then treat it under IFRS 15 just straight in PL if it is the fee related to that period it depends on the contract. Despite the guarantees settlement obligation is a fixed amount. Instead IFRS 9 introduces.

This is a new issue. Allow early adoption of the requirement to present fair value changes due to own credit on liabilities designated as at fair value through profit or loss to be presented in other comprehensive income. As part of the modification the entity pays a CU 150000 arrangement fee to the bank and a CU 50000 professional service fee to its lawyers.

5 Step 5 Recognise revenue when or as the entity satisfies a performance obligation 113. Any financial instruments that are currently accounted for under IAS 39 will fall within the IFRS 9s scope. IFRS 9 requires an entity to recognise a financial asset or a financial.

The objective of the entitys. IFRS 9 generally has to be applied by all entities preparing their financial statements in accordance with IFRS and to all types of financial instruments within the scope of IAS 39 including derivatives. IFRS 9 specifies how an entity should classify and measure financial assets financial liabilities and some contracts to buy or sell non-financial items.

IASB issues IFRS 9 Financial Instruments Hedge Accounting and amendments to IFRS 9 IFRS 7 and IAS 39 amending IFRS 9 to. If the commitment expires without making a loan the commitment fee is recognised as an expense. Paragraphs IFRS 9B542-3 give examples of fees that are and are not an integral part of the effective interest rate.

IFRS 9 paragraph B543a Commitment fees drawdown probable. And associated fees paid in a similar manner to the lender. The arrangement fee needs to be treated as a part of the effective interest method under IFRS 9 it means that your actual interest rate would be different from what you have in your contract because you need to count with all cash flows from the loan.

Under IFRS 9 the entire contract will have to be measured at FVPL in all but a few cases. This cost exception is not included in IFRS 9. Include the new general hedge accounting model.

IFRS 9 for corporates CLASSIFICATION AND MASURMNT Impairment Hedge accounting Other requirements Further resources. The Interpretations Committee received a request to clarify which fees and costs should be included in the 10 per cent test for the purpose of derecognition of a financial liability. IFRS 9 Final Standard In November 2009 the IASB issued IFRS 9 2009 the first milestone in the project to replace IAS 39.

Observation For equity instruments designated at FVTOCI under IFRS 9only. IFRS 9 replaces the rules based model in IAS 39 with an approach which bases classification and measurement on the business model of an entity and on the cash flows associated with each financial asset. Although there was no guidance prior to IFRS 9 there was a best practice related to.

IFRS 9 Amount deferred until loan is drawn down and the fee is included in the EIR.

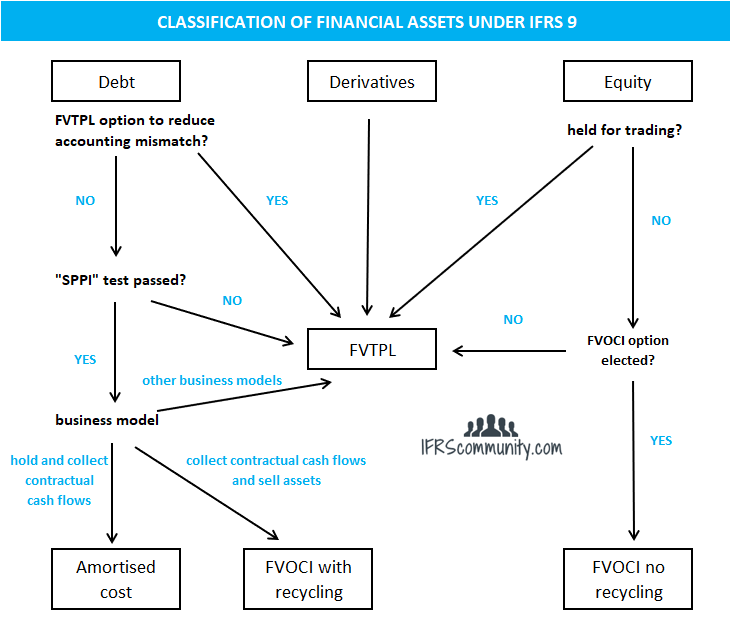

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com

Ifrs 9 Best Long Read Sppi Test Annual Reporting

Does Ifrs 15 Or Ifrs 9 Apply To Fees Charged To Customers By Lenders Bdo Australia

Financial Assets Under Ifrs 9 Two Key Tests Drive Classification Bdo Australia

Ifrs 13 Fair Value Measurement Lectures Notes Fair Value Accounting Student

2

2

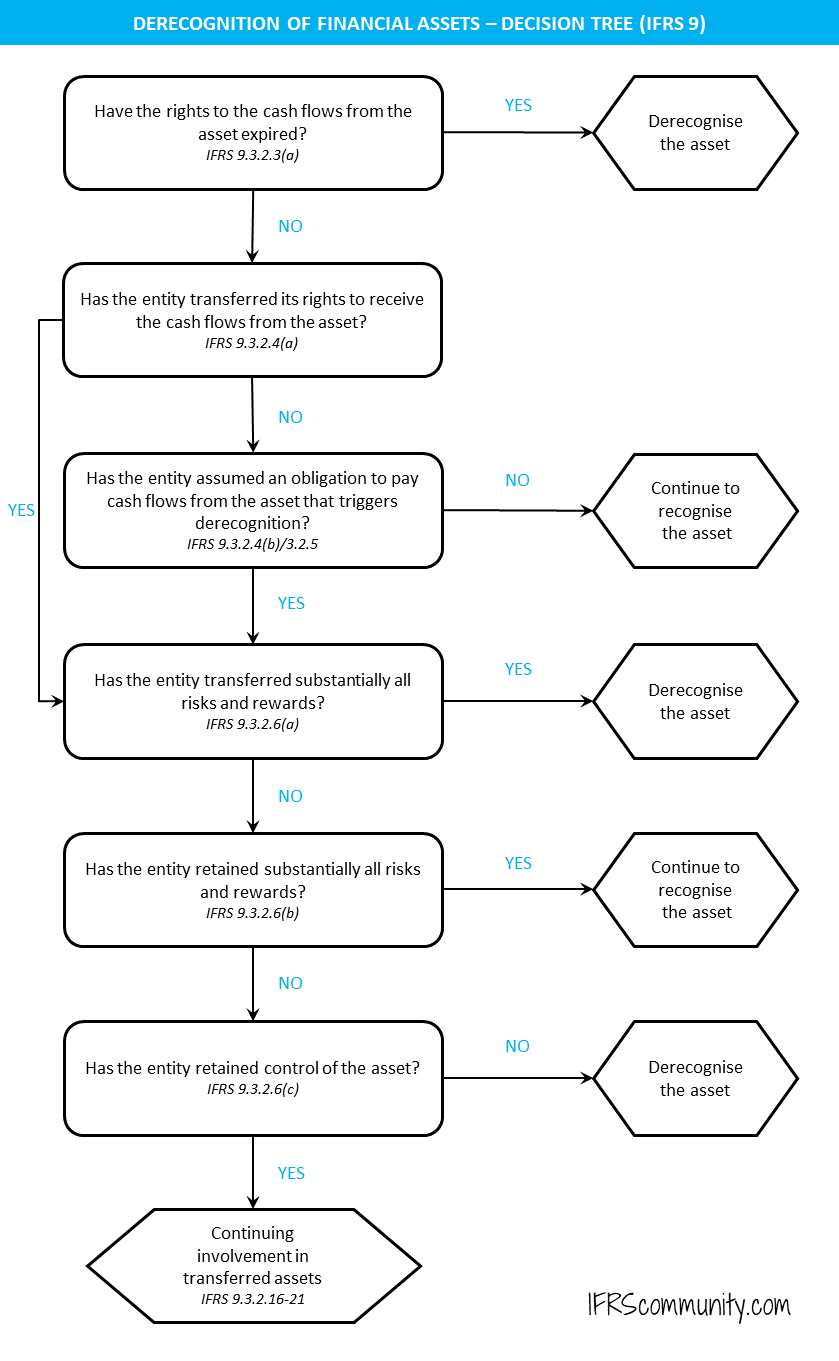

Ifrs 9 Transfer Right To Receive Cash Flows Annual Reporting

Ifrs 9 Classification And Measurement Of Financial Instruments Annual Reporting

Ifrs 9 The Sppi Test Explained By Example Annual Reporting

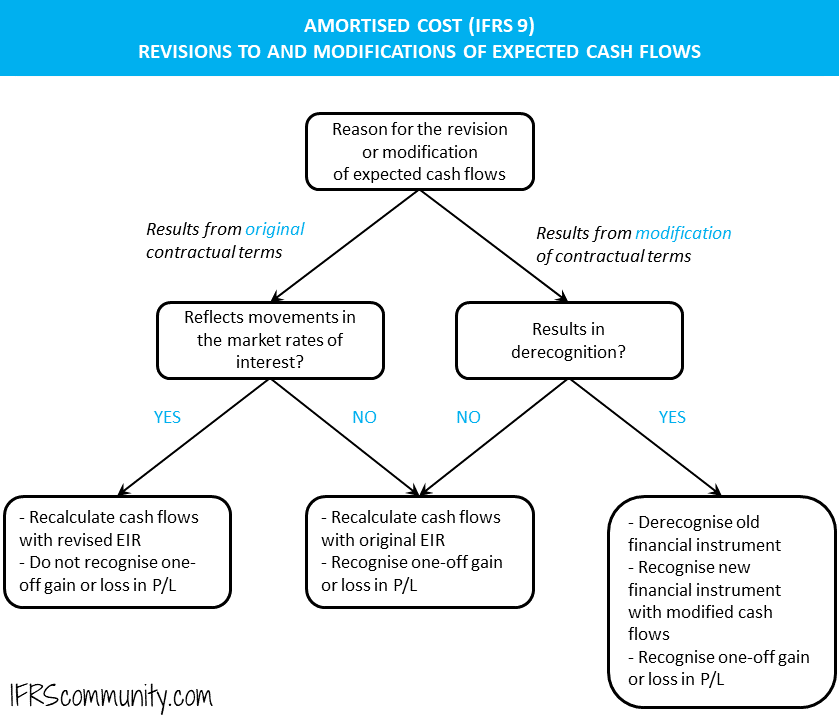

Amortised Cost And Effective Interest Rate Ifrs 9 Ifrscommunity Com

Financial Accounting Standards Ifrs 11 Joint Arrangements Financial Instrument Financial Accounting Joint

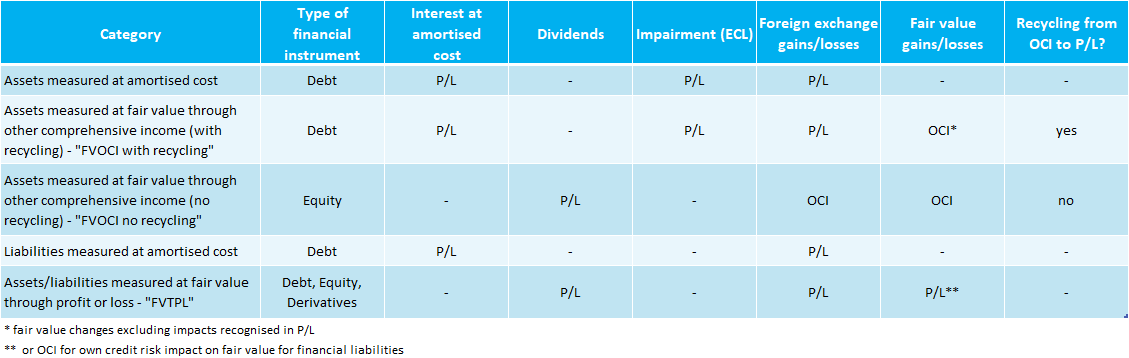

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com

Derecognition Of Financial Assets Ifrs 9 Ifrscommunity Com

{kind=link}

Posting Komentar untuk "Ifrs 9 Arrangement Fees"